“Manufacturing” is a broader concept that refers to the process of creating / producing goods through the transformation of raw materials or components into finished products.

Bill of Materials (BOM): Tally Prime allows you to create and manage Bill of Materials, which is a detailed list of all the components, raw materials, and sub-assemblies required to manufacture a finished product.

Cost Tracking: Manufacturing involves various costs such as raw materials, labor, overheads, and more. Tally Prime’s manufacturing features help in tracking and calculating these costs accurately, providing insights into the overall cost of production.

Manufacturing means converting raw materials into a finished product. In TallyPrime, you can record the process of manufacturing using features like:

- Bill of Materials (BOM)

- Manufacturing Journal

- Stock Items & Units

- Cost Tracking

Why Use Manufacturing in TallyPrime?

Using the manufacturing feature in TallyPrime helps you:

| Purpose | Benefit |

| Track material usage | Know how many raw materials were used |

| Record finished goods | Maintain correct stock of manufactured items |

| Calculate actual cost of production | Include all direct costs in finished product |

| Save time | Automated material consumption entries |

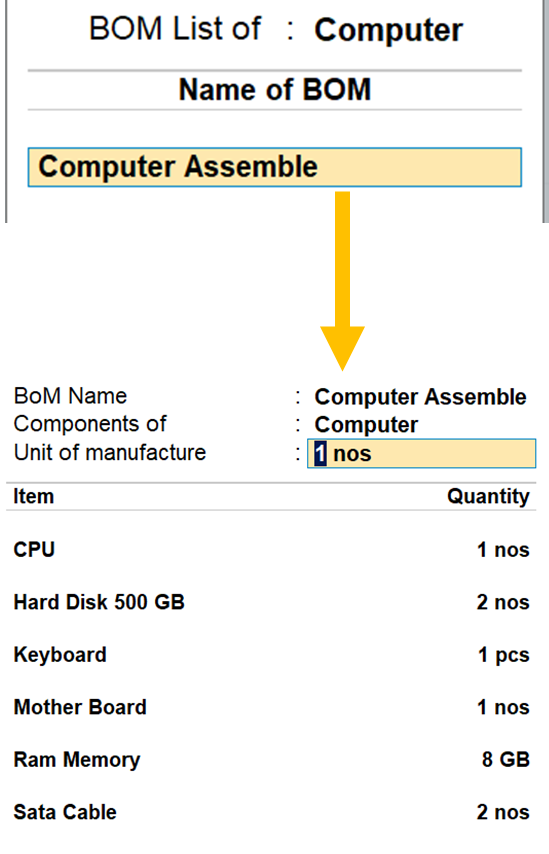

To make it efficient, TallyPrime uses a Bill of Materials (BOM), which is a predefined list of raw materials required to manufacture a finished product.

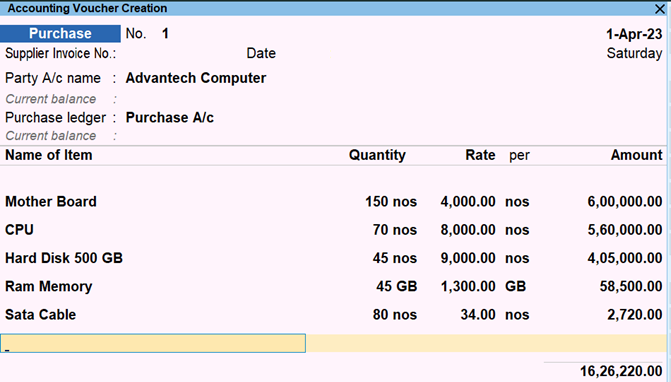

Step 1 Purchase Following Raw Material

GOT >> Vouchers >> Purchase

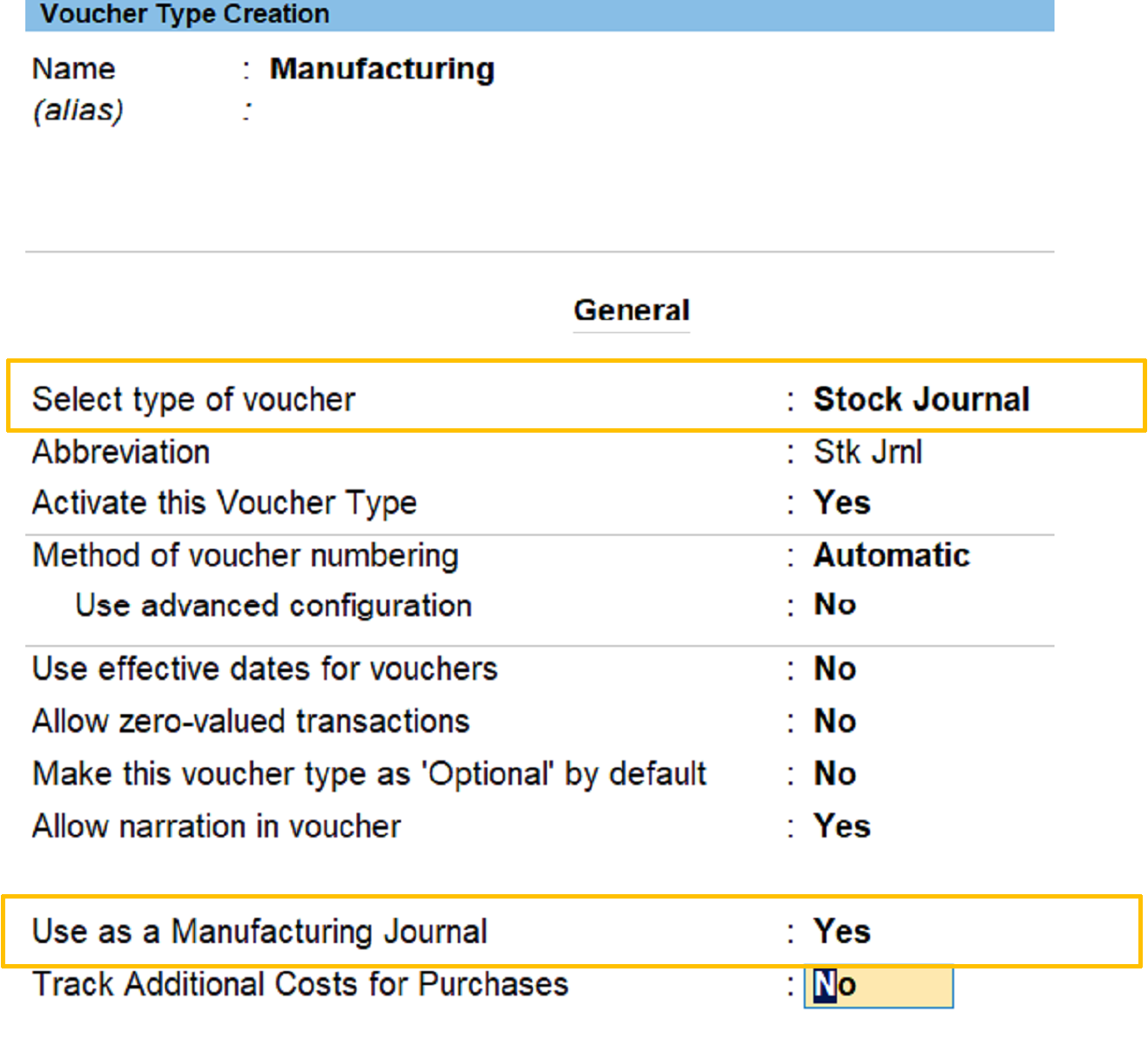

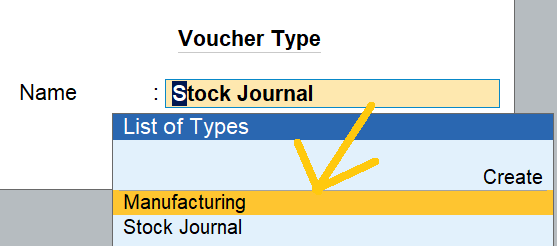

Step 2 Create A New Voucher

Gate Way Of Tally >> Create >>Voucher Type

- Select type of voucher

- Use as Manufacturing voucher journal

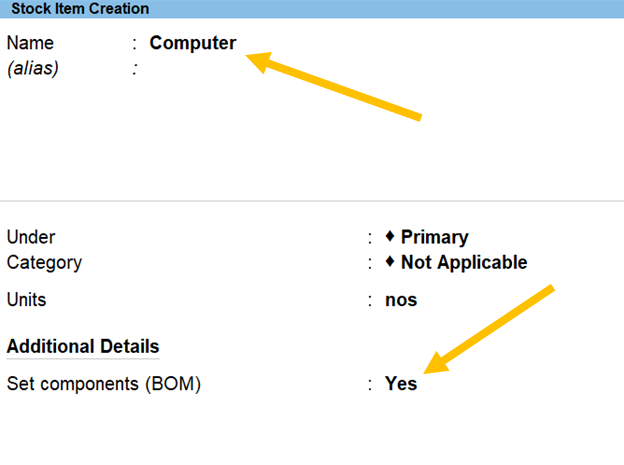

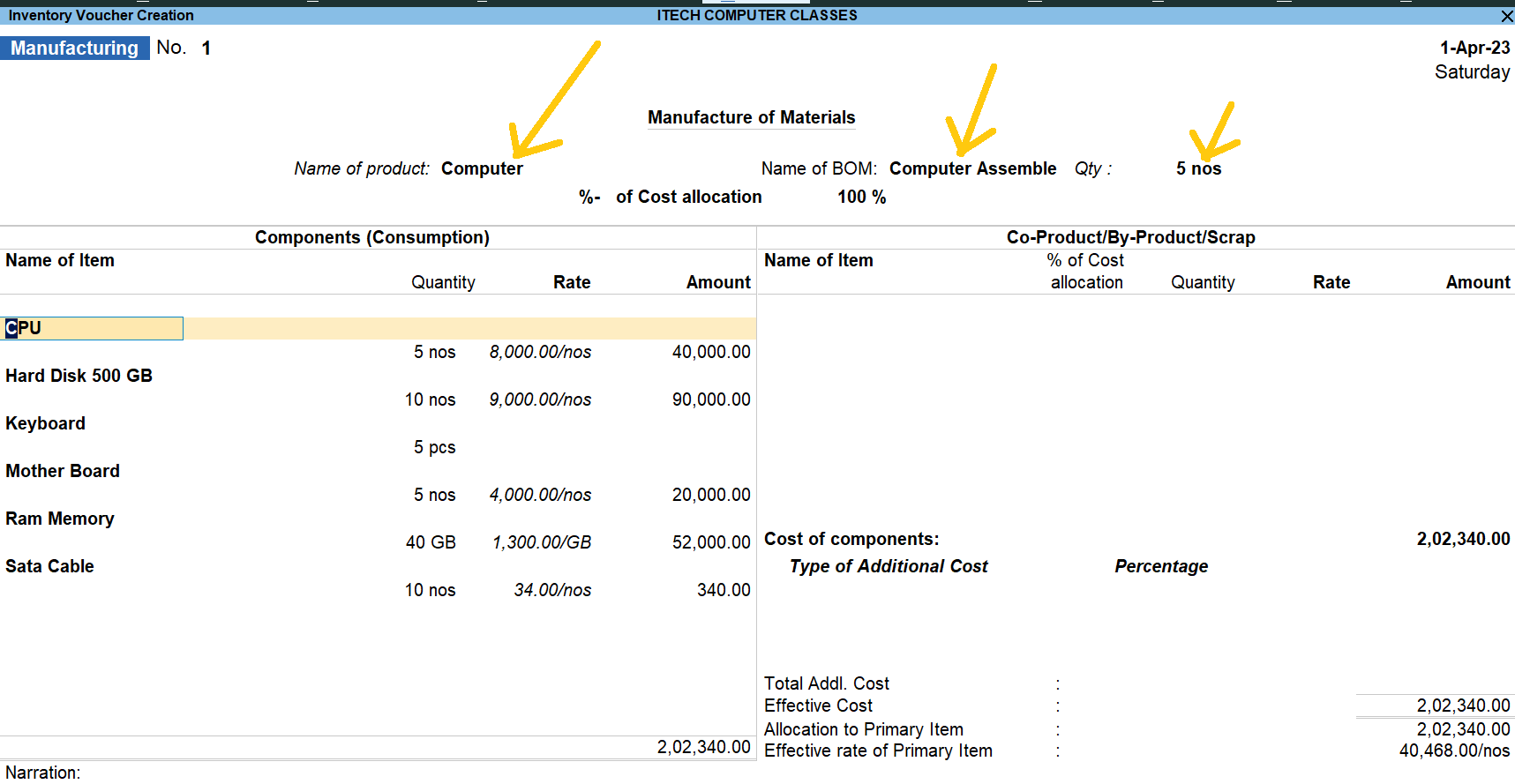

Step 3 Create Finishing Stock Item “Computer Assemble”

Set Up Components or Raw Materials Ratio Quantity

Step 4 Pass Manufacturing Voucher by Pressing ALT F7

Manufacturing Voucher will be like this

Example 1: Computer Assembling

Party: TechSource Traders

Raw Material Purchase:

| Item | Qty | Rate | Amount |

| CPU | 10 | ₹20,000 | ₹2,00,000 |

| Monitor | 10 | ₹10,000 | ₹1,00,000 |

| Keyboard | 10 | ₹1,000 | ₹10,000 |

| Mouse | 10 | ₹500 | ₹5,000 |

Total Purchase = ₹3,15,000

Production:

You assemble 5 Computer Sets using 5 of each component.

| Used Material | Qty Used |

| CPU | 5 |

| Monitor | 5 |

| Keyboard | 5 |

| Mouse | 5 |

Finished Product:

5 Computer Sets @ ₹63,000 each = ₹3,15,000

Balance Stock:

| Item | Opening | Used | Balance |

| CPU | 10 | 5 | 5 |

| Monitor | 10 | 5 | 5 |

| Keyboard | 10 | 5 | 5 |

| Mouse | 10 | 5 | 5 |

| Computer Set | 0 | — | 5 |

Example 2: Car Manufacturing

Party: AutoZone Parts Ltd.

Raw Material Purchase:

| Item | Qty | Rate | Amount |

| Car Engine | 5 | ₹1,50,000 | ₹7,50,000 |

| Car Body | 5 | ₹2,00,000 | ₹10,00,000 |

| Tyre Set | 5 | ₹25,000 | ₹1,25,000 |

| Paint Material | 5 | ₹5,000 | ₹25,000 |

Total Purchase = ₹19,00,000

Production:

Assemble 5 Cars

| Used Material | Qty Used |

| Car Engine | 5 |

| Car Body | 5 |

| Tyre Set | 5 |

| Paint Material | 5 |

Finished Product:

5 Cars @ ₹3,80,000 each = ₹19,00,000

Balance Stock:

| Item | Opening | Used | Balance |

| All Items | 5 | 5 | 0 |

| Car | 0 | — | 5 |

Example 3: Cake Manufacturing in a Bakery

Party: Fresh Bake Suppliers

Raw Material Purchase:

| Item | Qty | Rate | Amount |

| Flour | 50 kg | ₹40 | ₹2,000 |

| Sugar | 20 kg | ₹45 | ₹900 |

| Butter | 10 kg | ₹200 | ₹2,000 |

| Eggs | 100 | ₹10 | ₹1,000 |

| Boxes | 20 | ₹20 | ₹400 |

Total Purchase = ₹6,300

Production:

Bake 20 Cakes

| Used Material | Qty Used |

| Flour | 20 kg |

| Sugar | 10 kg |

| Butter | 5 kg |

| Eggs | 40 |

| Boxes | 20 |

Finished Product:

20 Cakes @ ₹315 each = ₹6,300

Balance Stock:

| Item | Opening | Used | Balance |

| Flour | 50 kg | 20 | 30 kg |

| Sugar | 20 kg | 10 | 10 kg |

| Butter | 10 kg | 5 | 5 kg |

| Eggs | 100 | 40 | 60 |

| Boxes | 20 | 20 | 0 |

| Cakes | 0 | — | 20 |